The S&P 500 notched a third consecutive week of gains as the index broke and held above its 50-day moving average. Investors were treated to another dose of first-quarter corporate earnings. Disney, Uber, and ARM results were disappointing, while Taiwan Semiconductor’s monthly revenues beat expectations and sparked a rally in the Semiconductors. Over 80% of the S&P 500 companies have posted their quarter earnings, and earnings growth looks well above pre-earnings season estimates. Sector performance over the week was led by the Utilities, Financials, Materials, and Consumer Staples. This change in market leadership from technology to other sectors shows that the market rally is trying to broaden. This broadening out can also be seen with interest in European and Asia equities, where central bank policy will likely become more accommodative in the next couple of months. The Bank of England kept its policy rate in place but did indicate that it is poised to cut rates in the near future.

The S&P 500 gained 1.9%, the Dow rose by 2.2%, the NASDAQ added 1.1%, and the Russell 2000 increased by 1.2%. US Treasuries lost some ground this week, but trade seemed fairly quiet relative to the last several weeks. Interestingly, this relatively quiet market came as the Treasury auctioned $125 billion in Treasuries. The auction results were mixed, with the 3-year and 10-year auctions getting tepid interest, while the 30-year saw decent interest. The 2-year yield increased by six basis points to 4.87%, while the 10-year yield was unchanged on the week at 4.50%. Oil prices were little changed for the week closing at $78.20 a barrel. Gold prices increased by 2.8% to close at $2374.80 an Oz. Copper prices bounced back this week, gaining $0.11 to $4.66 per Lb. The US Dollar index increased by 0.2% to 105.3.

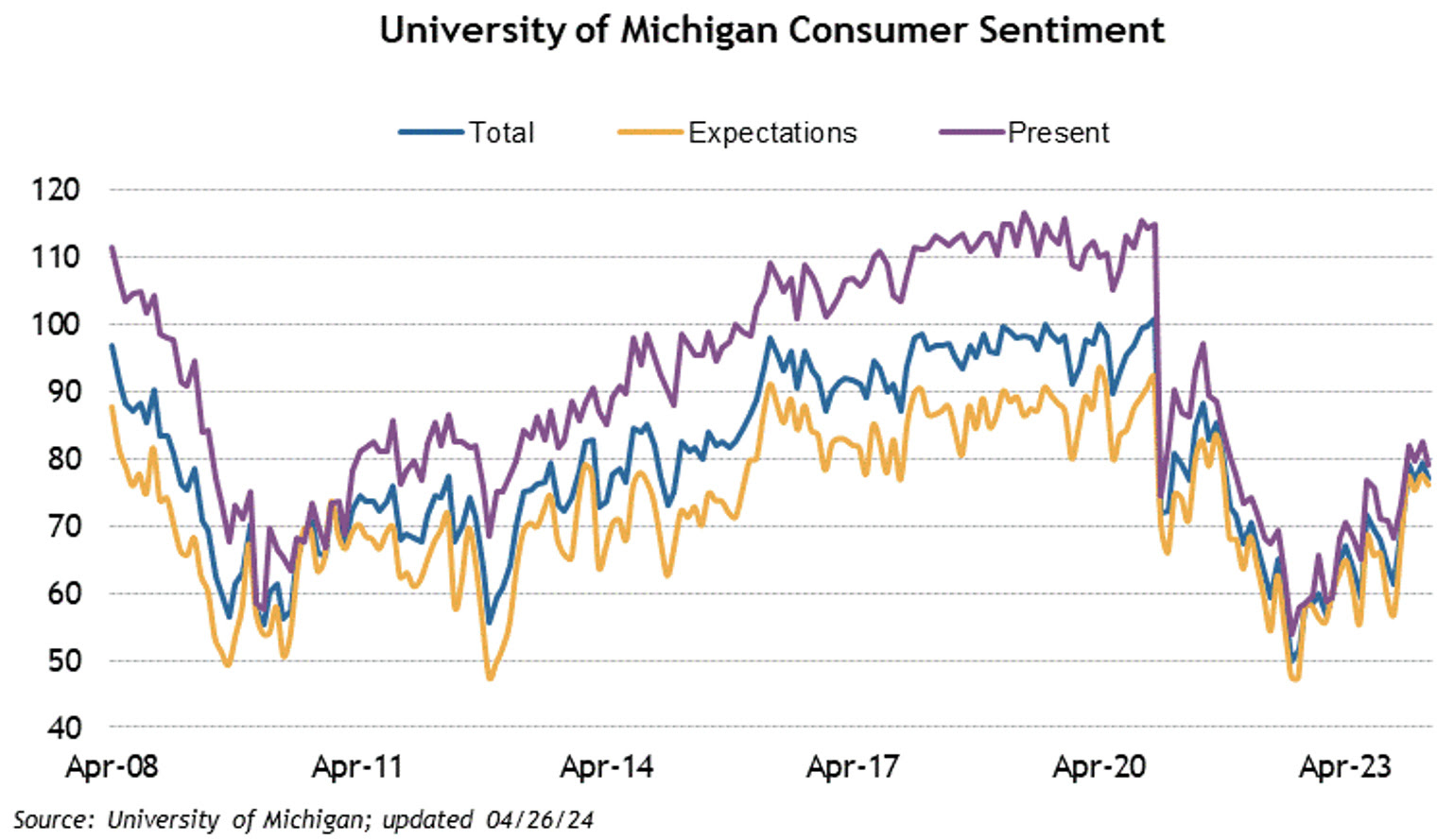

The economic calendar was light but we did have a number of Fed Officials that spoke throughout the week. Bowman and Kashkari came across as the most hawkish, while Daly, Collins, and Williams reiterated the idea of higher for longer, with a rate cut coming sometime this year after more economic data has been assessed. The preliminary reading of the University of Michigan’s Consumer Sentiment Index caught some attention as it showed a troubled consumer who is worried about inflation, high interest rates, and employment. The index fell to a six-month low at 67.4, well below the prior reading of 77.2. The consumer has so far been resilient and continuing to spend; if this changes, so too will the narrative of a soft landing. Coming off the weaker-than-expected employment data from the prior week, investors saw an uptick in Initial Jobless claims to 231k, up 22k from the prior week. Similarly, Continuing Claims increased by 17k to 1.785M.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involve risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.